GCCs didn’t become the backbone of enterprise finance by accident. Over the last decade, they centralized transactions, standardized controls, and scaled operations across time zones.

On paper, finance should have become sharper. In practice, a different problem emerged.

Many finance shared-services and GCC programs report 25–50% cost reduction, and some targeted transformations have delivered up to 75% lower finance TCO when combined with automation and process redesign.

Where Finance Actually Sits in a GCC Model

In most global enterprises, finance does not sit where decisions are made. Commercial teams restructure deals, operations adjust fulfilment, and customers settle through non-standard routes—all in real time.

In many global enterprises, transaction data reaches central finance 15–20 days after the underlying business decision once local approvals, fulfilment updates, and settlement flows across regions have run their course. This is not a speed problem. It is a structural lag created by geography, approval chains, and fragmented systems.

The Reality Gap: Even when data lands earlier, it often isn’t trusted until it has been validated and reconciled, which effectively pushes finance’s "real" view of the business closer to month-end.

Finance doesn’t sit where decisions are made. It sits where decisions are explained.

When Margin Problems Hide in Plain Sight

Consider the "Double-Discount" trap. A sales team in APAC offers a volume discount to close a deal, while marketing runs a rebate program targeting the same customer.

Because GCCs often reconcile revenue streams separately and periodically, an unintended pricing or discount configuration can quietly erode margin. For example, an effectively 40% customer discount on a product with a typical 35% gross margin might not be detected until revenue is recognized and the period is closed. This pattern of operational issues surfacing only at close reflects what finance effectiveness benchmarks consistently show about lagging visibility.

- The Impact: According to MGI Research, 42% of enterprises suffer from material revenue leakage. Even a 5–7 percentage-point erosion in gross margin on a high-volume customer can translate into a multi-million-dollar leak, and it often stays invisible until central finance reconstructs what happened.

The issue wasn’t discounting. The impact only became visible after revenue was already booked.

Accuracy Without Authority

Finance is accountable for accuracy but rarely empowered to intervene. There is a quieter tension in many GCC models: Business teams own decisions; GCC finance owns accuracy.

When something drifts mid-cycle, finance raises flags and corrects the numbers, but rarely has the mandate to intervene while a decision is still reversible.

Because most GCC setups still measure finance on SLA adherence, closing on time, posting accurately, the organization unintentionally trains finance to excel at post-mortems. The system rewards "explaining what happened" far more than "stopping it in flight."

The Multi-Currency Blind Spot

At GCC scale, a 1% exception rate is not a rounding error. It is a full-time team firefighting exceptions. Consider a GCC handling 20+ currencies where a minor misconfiguration in a new entity’s hedging logic goes unnoticed for weeks.

By the time the periodic close begins, the cumulative FX impact can easily become a seven-figure variance that is effectively impossible to hedge away retroactively. The issue was not the initial error; it was discovering it when the transactions were already locked in.

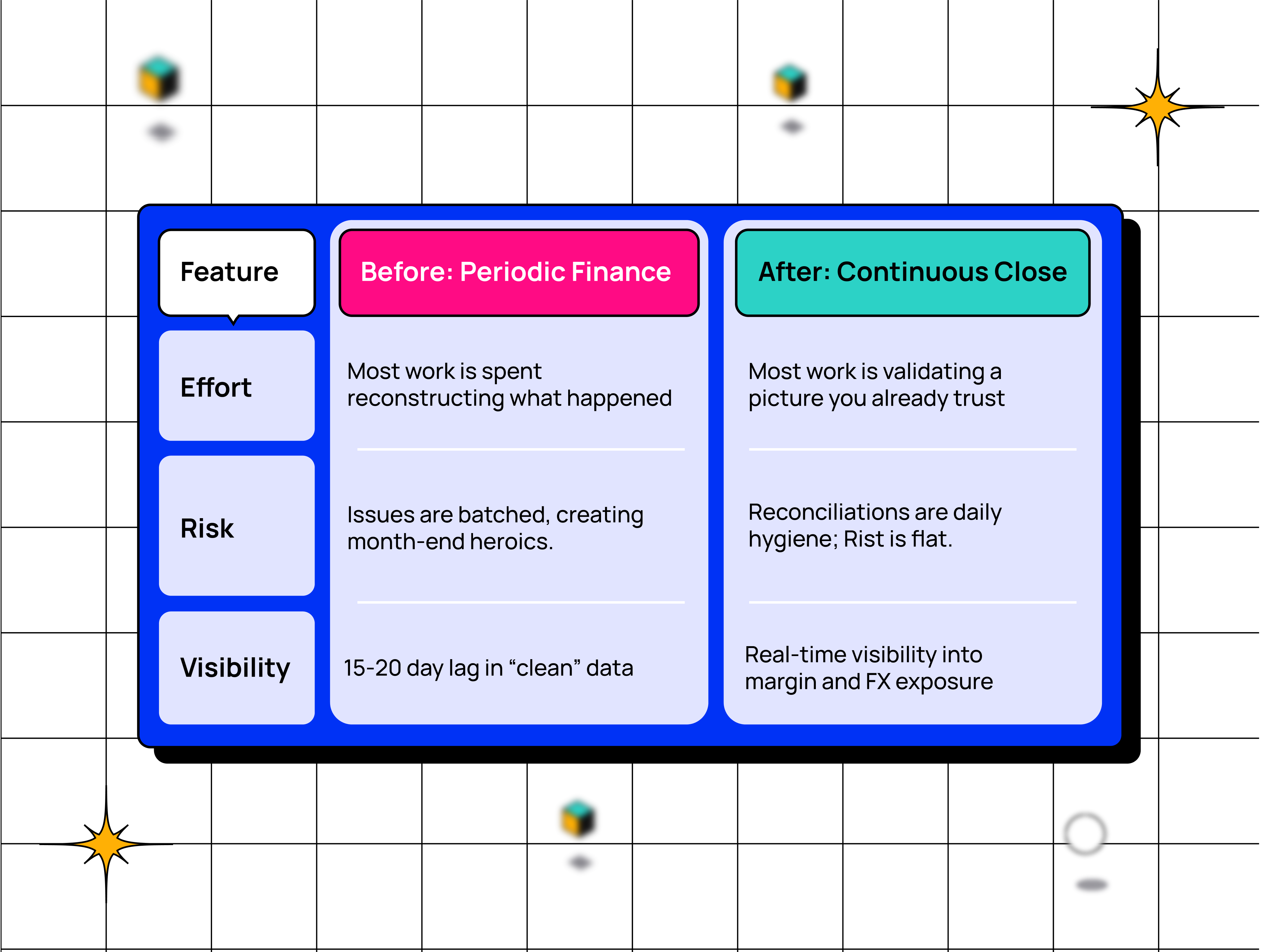

When issues surface only at period-end, finance is forced into explanation mode. Continuous close exists to break that cycle.

Why "Continuous Close" is the GCC's Next Phase

Continuous close is often misunderstood as just "closing the books faster." In a GCC context, it is about timing and relevance: moving reconciliations and validations into the flow of business so finance can act while transactions are still in motion.

When sub-ledgers (AP, AR, Fixed Assets) remain clean throughout the period, the general ledger becomes a summary layer rather than a forensic exercise at month-end.

The Real Takeaway

GCCs did not break finance; they exposed a gap between how the business now operates – continuously, in real-time, and how finance still works – periodically, after the fact. Centralization made that gap visible; scale made it painful.

The next phase of GCC finance is not about faster closes or larger teams. It is about shrinking the distance between where financial signals appear and where action is taken. That is the shift continuous close enables, and it is why GCCs sit at the center of this conversation, whether enterprises are ready to admit it or not.

Once finance is centralized at scale, latency stops being tolerable. It becomes visible, measurable, and expensive. Moving toward a continuous model is no longer an “innovation” project. It is the only way finance stays relevant to the decisions that actually drive the business.

Bluecopa supports this shift by helping GCC and enterprise finance teams keep sub-ledgers continuously clean, reconciled, and trustworthy throughout the period, so margin, FX, and exception risk surface early enough to act, and not explain outcomes after the fact.